A hot tub can make your backyard a relaxing retreat with therapeutic benefits and a place for family and friends. However, quality hot tubs often cost $4,000 to $20,000 or more, making upfront payment challenging for many homeowners.

Hot tub financing becomes a viable option in this situation. Financing enables consumers to spread the cost into manageable payments rather than paying the entire amount upfront, allowing them to start enjoying the hot tub immediately.

To help you navigate these decisions, this comprehensive guide covers everything you need to know about hot tub financing, moving step by step through available options, interest rates, approval requirements, benefits, potential risks, and expert tips for securing the best deal.

What Is Hot Tub Financing?

Hot tub financing is a payment option that allows customers to purchase a hot tub through installment loans or credit plans rather than paying the full amount up front.

Typically, buyers apply for financing through:

- Hot tub retailers

- Personal loan providers

- Credit card companies

- Home improvement financing programs

After approval, the lender pays the retailer, and the buyer repays the loan over time through monthly payments plus interest (in most cases). This financing model helps homeowners enjoy luxury amenities without straining their immediate cash flow.

Why Many Homeowners Choose Hot Tub Financing

Hot tubs are considered premium lifestyle investments, and financing makes them accessible to more households.

Immediate Enjoyment

Financing lets buyers install a hot tub right away, rather than waiting years to save. This immediate access enables them to enjoy relaxation, hydrotherapy, and outdoor comfort sooner.

Flexible Payment Plans

Many financing options offer flexible terms, usually from 12 months to 7 years. Buyers can choose a schedule that fits their budget. Flexible plans make large purchases manageable.

Preserve Savings

Financing spreads the cost over smaller payments, helping buyers keep savings intact for emergencies. This preserves financial security while making the purchase.

Potential Promotional Offers

Some retailers offer promotional financing, like 0% APR for qualified buyers. Paying within this period may mean no interest, making financing more affordable.

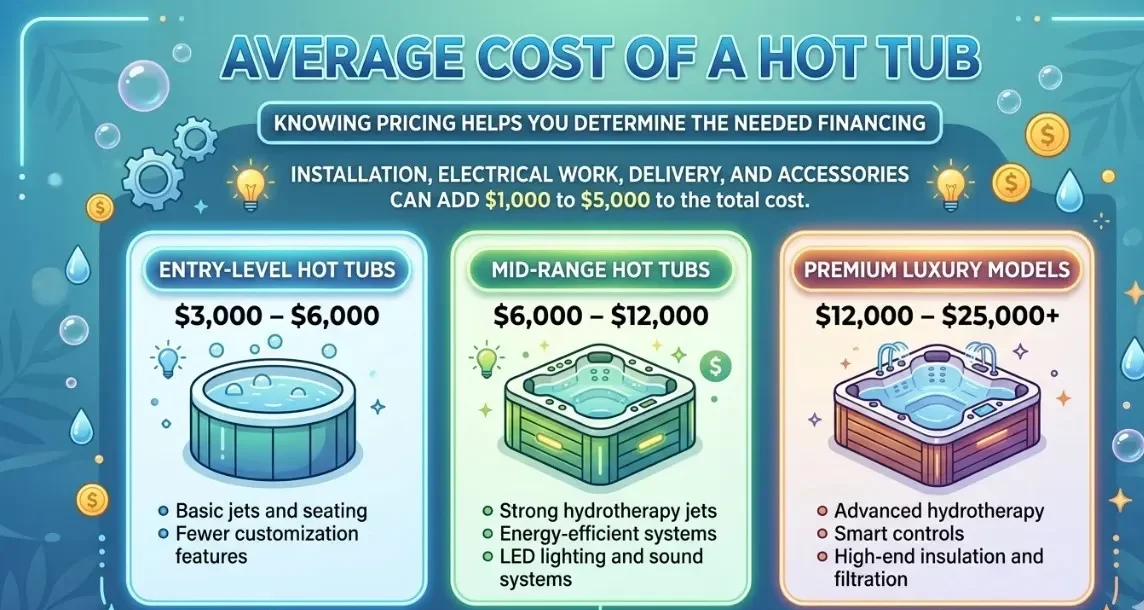

Average Cost of a Hot Tub

Knowing pricing helps you determine the needed financing. Installation, electrical work, delivery, and accessories can add $1,000 to $5,000 to the total cost.

Entry-Level Hot Tubs

- Cost: $3,000 – $6,000

- Basic jets and seating

- Fewer customisation features

Mid-Range Hot Tubs

- Cost: $6,000 – $12,000

- Strong hydrotherapy jets

- Energy-efficient systems

- LED lighting and sound systems

Premium Luxury Models

- Cost: $12,000 – $25,000+

- Advanced hydrotherapy

- Smart controls

- High-end insulation and filtration

Types of Hot Tub Financing Options

There are several ways to finance a hot tub. Each has advantages based on your credit, goals, and preferred repayment timeline.

1. Dealer Financing

Many hot tub retailers work with lenders for in-house financing. These options offer fast approval, easy applications, and possible promotional rates for qualified buyers.

Pros

A main advantage is quick approval, enabling buyers to secure funding quickly. Special promotional deals can also make purchases more affordable, offering convenience for many customers.

Cons

Potential drawbacks include limited lender options and possibly higher interest rates after promotions, which can increase overall cost.

2. Personal Loans

Personal loans from banks, credit unions, or online lenders are another option for financing a hot tub. Loan amounts typically range from $2,000 to $50,000, with terms from 2 to 7 years and rates from 6% to 36%, depending on credit.

Pros

This financing option offers several advantages. One is fixed monthly payments, making budgeting easier and more predictable. No collateral is required, and funds can be used for any borrower.

Cons

Disadvantages include higher interest rates for lower credit scores and stricter approval based on creditworthiness.

3. Home Equity Loans or HELOC

Homeowners can use home equity to finance a hot tub, often for larger backyard projects.

Pros

Benefits include lower interest rates and higher borrowing limits than most personal loans, which help fund major purchases.

Cons

This financing option has drawbacks; borrowers should be aware of one key risk: their home could be lost as collateral if payments are missed. The approval process is also longer and often requires more documentation than other loans.

4. Credit Card Financing

A credit card with a 0% introductory APR can be used for short-term repayment. Benefits include instant access to funds and potential rewards, such as points or cashback on purchases.on purchases.

Pros

The main advantages include instant access to funds, reward points, or cash back.

Cons

However, there are risks to consider. Interest rates can rise sharply once the promotional period ends, increasing the cost of carrying a balance. Additionally, using a significant portion of available credit can affect credit utilisation, which may impact your overall credit score.

Typical Interest Rates for Hot Tub Financing

Interest rates vary by credit score, lender, and method. Higher scores typically mean better rates and terms. Borrowers with higher credit scores typically qualify for lower interest rates and better repayment terms.

| Credit Score | Estimated APR Range |

|---|---|

| Excellent (750+) | 6% – 10% |

| Good (700–749) | 10% – 18% |

| Fair (650–699) | 18% – 25% |

| Poor (Below 650) | 25% – 36% |

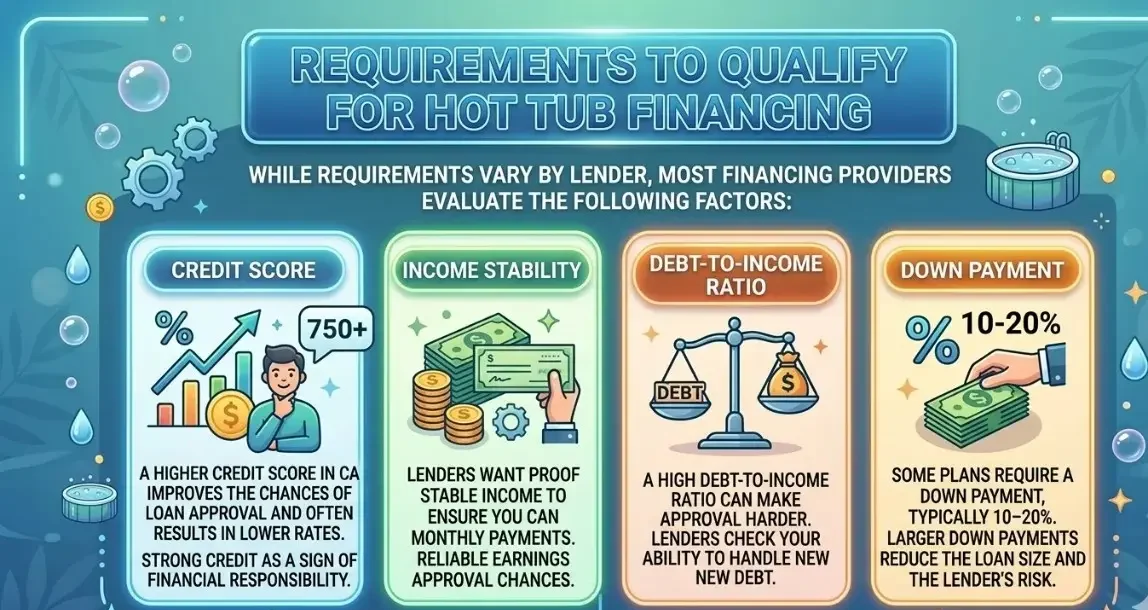

Requirements to Qualify for Hot Tub Financing

While requirements vary by lender, most financing providers evaluate the following factors:

Credit Score

A higher credit score in CA improves the chances of loan approval and often results in lower rates. Lenders see strong credit as a sign of financial responsibility. sponsibility.

Income Stability

Lenders want proof of stable income to ensure you can manage monthly payments. Reliable earnings boost approval chances.

Debt-to-Income Ratio

A high debt-to-income ratio can make approval harder. Lenders check your ability to handle new debt.

Down Payment

Some plans require a down payment, typically 10–20%. Larger down payments reduce the loan size and the lender’s risk.

How to Get the Best Hot Tub Financing

A strategic approach saves money over the life of the loan—the loan term. Lower prices reduce what you finance.

Compare Multiple Lenders

Before financing, compare at least three lender offers. This reveals the best interest rates, terms, and repayment options, allowing you to make a more informed, cost-effective decision.

Check Promotion

Retailers may offer promotional deals, such as 0% APR. like 0% APR. Check for current offers before finalising a purchase.

Improve Your Credit Score First

Pay off small debts and raise your credit score before applying. Higher credit improves approval odds and rates.

Choose Shorter Loan Terms

Shorter loan terms mean higher monthly payments but lower total interest. Pay debt faster and cut costs if possible.

Negotiate the Total Purchase Price

Many buyers overlook that the price of the hot tub itself is negotiable. Negotiating the purchase price can lower both the upfront cost and the financed amount. This approach maximises value and can make financing more manageable.

Pros and Cons of Hot Tub Financing

Understanding both sides ensures buyers make informed financial decisions.

Advantages

- Makes luxury purchases more affordable

- Preserves savings and emergency funds

- Flexible payment plans

- Possible interest-free promotional offers

Disadvantages

- Interest increases the total purchase cost.

- Missed payments may affect your credit score.

- Long repayment periods can extend financial commitments.

Final Thoughts

Investing in a hot tub can significantly enhance your home’s comfort, relaxation, and entertainment value. However, the financial commitment should always be approached carefully. Hot tub financing provides a flexible pathway to enjoy luxury without a large upfront payment.

By comparing lenders, understanding interest rates, and calculating long-term costs, homeowners can choose a financing option that aligns with their budget and financial goals. The key is to prioritise affordability, transparency, and responsible repayment planning. When done correctly, financing can turn a dream backyard spa into a practical and rewarding investment.

Frequently Asked Questions (FAQs)

Can I finance a hot tub with bad credit?

Yes, some lenders offer bad-credit financing options, but interest rates may be significantly higher.

How long can you finance a hot tub?

Most financing terms range between 12 months and 7 years, depending on the lender and loan type.

Is 0% financing for hot tubs really interest-free?

Yes, but only if the loan balance is paid in full within the promotional period. Otherwise, deferred interest may apply.

Do hot tub dealers offer financing?

Many hot tub retailers offer in-house financing or partner with lenders, making it easy to apply during the purchase process.

Does financing a hot tub affect my credit score?

Yes. Applying for financing may result in a temporary credit inquiry, and your payment history will affect your credit score over time.

{kind=link}

{kind=link}